Three years ago, a 32GB DDR5 kit cost $80. Today the floor is $375, if it’s in stock at all.

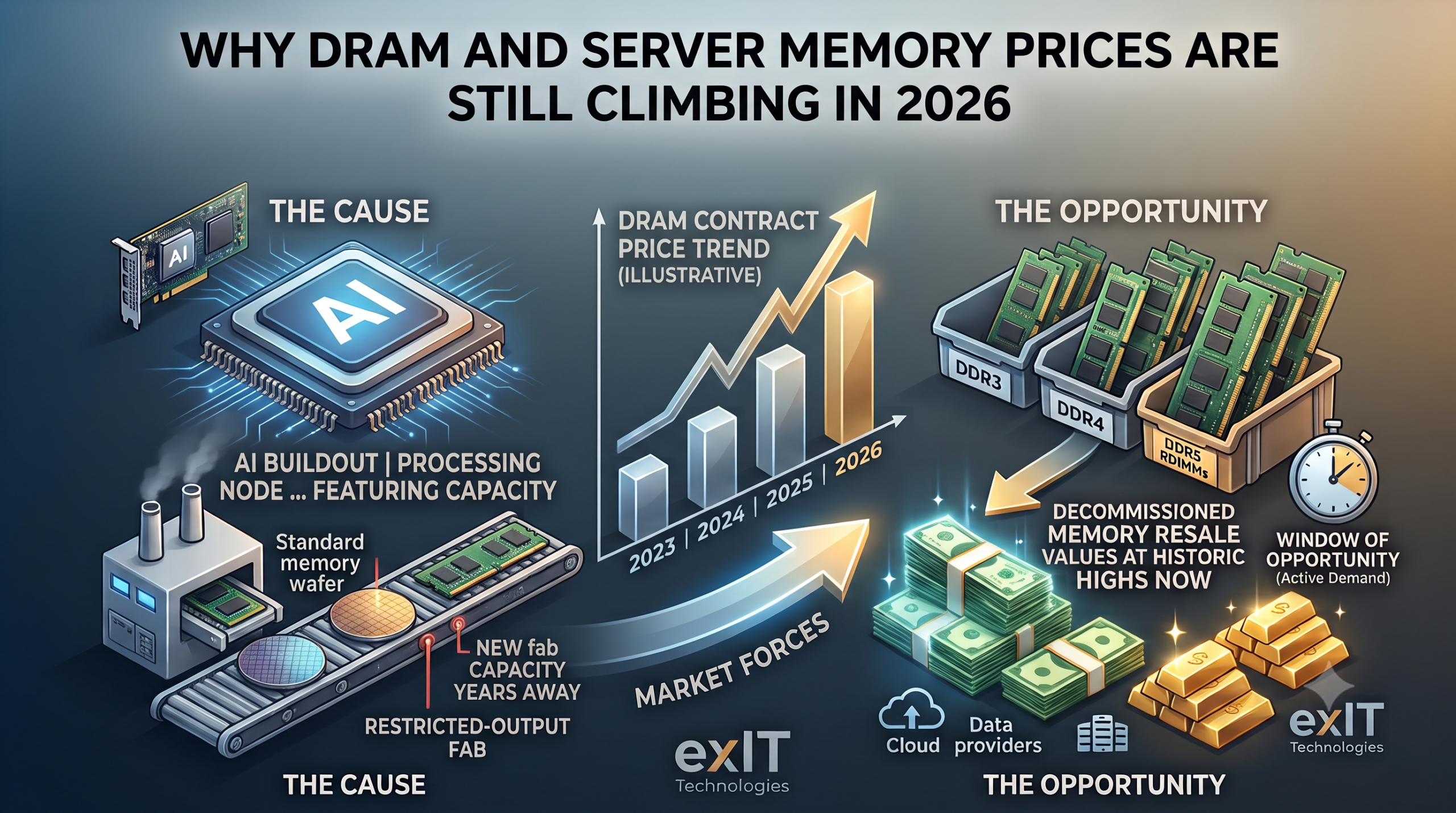

This is not just a spike. The memory market has repriced permanently. TrendForce’s June 2026 data puts Q1 conventional DRAM contract prices up 93-98% quarter over quarter. That’s the largest quarterly increase ever recorded. The stakes are high, and misreading the market can lead to massive financial losses.

Here’s what the underlying data of the memory market actually shows, and what it means if you’re making procurement or disposition decisions right now.

Fast Facts: Memory Market Trends For 2026

- DRAM contract prices rose 93-98% QoQ in Q1 2026, with Q2 forecast to add another 58-63% QoQ, according to TrendForce. These changes are driven by AI infrastructure investment.

- Meaningful new DRAM supply increases won’t arrive until late 2027 or 2028, at the earliest.

- NAND Flash contract prices are forecast to rise 70-75% QoQ in Q2 2026, outpacing DRAM’s rate of increase for the first time in this cycle, according to TrendForce.

- If you’re holding decommissioned DDR3, DDR4, or DDR5 server memory, secondary-market resale values are unusually strong. That window won’t stay open indefinitely.

- Raymond James analyst Karl Ackerman has flagged a potential mid-2026 price peak, but that signals a deceleration in price growth, not a reversal. Contract prices aren’t declining yet.

What’s Causing Memory Prices To Increase?

AI inference buildout is consuming manufacturing capacity that used to produce conventional server and desktop memory.

As demand for LLM training and AI inference grows, cloud service providers are shifting deployment priorities from general-purpose servers toward AI-specific servers. The result has been memory procurement needs beyond HBM3e and LPDDR5X to include RDIMMs across a broader range of capacities. The DRAM supply crunch that started in the AI-specific product lines is now bleeding into conventional server memory that your data center actually runs on.

Cloud providers are exacerbating this through their purchasing behavior. CSPs’ willingness to accept price increases has prompted other customers to follow in order to secure allocations. When Microsoft, Google, and AWS are willing to sign multi-quarter agreements at elevated prices to lock in HBM3e and high-capacity RDIMM supply, every other buyer gets pushed down the queue. They have to pay more for what’s left as well.

Supplier inventories are approaching depletion, with shipment growth now reliant solely on wafer output increases. The industry is running on real-time production. Any disruption to wafer output (a yield issue, a fab slowdown, a logistics problem) shows up in contract prices within weeks.

The NAND side of the equation is following the same logic. Suppliers focused on profit maximization are shifting supply from client SSDs to data center SSDs. Enterprise buyers are competing for a limited pool and consumer buyers are left with a smaller slice of the pie than ever.

The Numbers: Where Memory Prices Actually Stand Q3 2026

Contract prices are what data centers and OEMs negotiate quarterly. Spot prices are the open-market rate for one-off orders, and they move first. Right now, both are trending in the same direction.

| Metric | Mid-2026 Status | Source |

| Conventional DRAM contract price, Q1 2026 QoQ | +93-98% | TrendForce, June 2026 |

| Conventional DRAM contract price, Q2 2026 forecast QoQ | +58-63% | TrendForce, March 31, 2026 |

| NAND Flash contract price, Q2 2026 forecast QoQ | +70-75% | TrendForce, March 31, 2026 |

| Total memory industry revenue, Q1 2026 QoQ | +81%, to $97B | TrendForce, June 2026 |

| DDR5 32GB kit, Oct. 2025 vs. June 2026 | ~$100-200 → $375 minimum | Tom’s Hardware |

| DDR4 32GB kit, Oct. 2025 vs. Jan. 2026 | ~$60-90 → ~$150-180 | Tom’s Hardware |

| New supply (CXMT, YMTC) meaningful volume | Not expected until late 2027-2028 | TrendForce |

The consumer-facing numbers tell the same story. A 32GB DDR5 kit that sold for $100-$200 in October 2025 now starts at $350 if it’s even in stock. DDR4 isn’t a safe harbor either. The same DDR4 kits that sold for $60-$90 in October 2025 were already running $150-$180 by January 2026.

How To Read The Signals Of The Memory Market

In early June, Raymond James analyst Karl Ackerman triggered a memory stock selloff when he published a note stating that DRAM and NAND average selling prices are expected to peak in mid-2026, before declining for two consecutive quarters starting early next year. Micron shed nearly $95 billion in market cap in a single day. South Korean and Taiwanese memory stocks followed.

Ackerman is forecasting a deceleration in the rate of price increases, not a full-on collapse. He believes the impact of a peak may be less severe than in typical down cycles because long-term supply agreements between chipmakers and customers could help cushion the industry from a sharp correction.

Despite this small decline, Micron announced a 346% increase in revenue year over year at the end of June and its stock hit an all-time high. Price-adjustment or not, Micron has been able to charge more and more for its products, and its stock can’t stay on its shelves.

What TrendForce’s actual contract data shows is more nuanced. DRAM’s rate of increase is slowing, going from 93-98% QoQ in Q1 to a forecast 58-63% in Q2. That’s still 58-63% in a single quarter. NAND Flash contract prices are projected to rise 70-75% QoQ in Q2, faster than DRAM’s pace and the first time in this cycle that NAND has outpaced DRAM on a quarterly basis.

TrendForce’s May 29 update noted that PC DRAM spot prices were stabilizing close to May levels through June as the Q2 contract negotiation cycle concluded. Spot-buyer hesitation at current prices is still present, but it reflects demand destruction. Some buyers are pulling back because they can’t absorb the cost.

A deceleration in price growth is not the same as prices declining. If you’re waiting for 2024 pricing to return, you’re waiting for a market structure that no longer exists.

New Supply Isn’t On The Way Until 2027 Or Later

Building new semiconductor fab capacity takes years, making it a risky bet for any manufacturer.

Suppliers are expected to rely primarily on process migrations to expand bit output in 2026, given the tight supply environment and the time required for new cleanroom construction. Samsung and SK Hynix have both signaled they won’t pursue aggressive fab expansion. The economics favor running existing lines at maximum utilization on the highest-margin products. They’ll produce more HBM and high-capacity server DRAM, not the DDR4 or entry-level DDR5 your refresh cycle depends on.

Chinese memory manufacturers ChangXin Memory Technologies (CXMT) and Yangtze Memory Technologies (YMTC) are ramping production capacity, but meaningful volume isn’t expected until late 2027 at the earliest. Entity List restrictions continue to limit CXMT’s access to the most advanced process nodes, which constrains how quickly they can scale into the server DRAM market where the shortage is most acute.

TrendForce and IDC both conclude that meaningful new production capacity from Micron’s Idaho fab, Samsung’s Texas facility, and SK Hynix’s Indiana packaging plant will not reach volume output before late 2027 or 2028.

What This Means If You’re Sitting on Surplus or Decommissioned Memory

Secondary-market pricing on pulled server and desktop RAM tracks new-memory pricing with a lag. When new DDR4 RDIMMs are trading at prices that would have seemed impossible two years ago, the pulled DDR4 units you have in bins from your last decommission are worth more than you think.

Organizations decommissioning servers now have a strong case for prioritizing memory recovery as part of the ITAD process. DDR3 still moves. DDR4 ECC is in active demand. DDR5 RDIMMs pulled from Gen 5 servers are particularly strong.

If you’re holding pulled server or desktop RAM from a recent refresh, this is a good time to get a quote rather than let it sit. The market has created a window. How long it stays open depends on whether the spot-buyer hesitation develops into something more sustained, or whether Q3 CSP earnings calls confirm continued AI-driven procurement pressure and stabilize prices at current levels.

The memory in your storage room isn’t waiting for a better market because that market is already here. You can cash in on your unused memory before the market structure shifts again.